Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

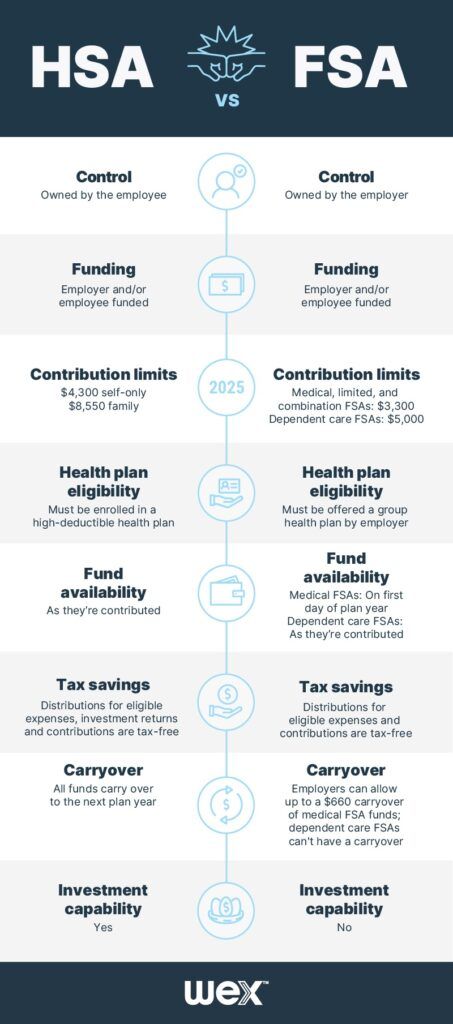

Participating in a health savings account (HSA) or flexible spending account (FSA) is a great way to save money. Below, we’ve outlined the key differences of an HSA vs. FSA so you can see how they work, the advantages to each, and why you should participate in them.

An HSA is an individually owned benefits plan funded by you or your employer that lets you save on purchases of eligible expenses. You must be enrolled in a high-deductible health plan (HDHP) to be eligible, which lowers you insurance premiums.

Health savings accounts have a triple-tax advantage, meaning distributions for qualified medical expenses and investment returns are tax-free, and contributions are tax-deductible. Health savings account funds can be invested for potential growth of your HSA funds.

Our HSA comes with a low investment threshold, and our online account and mobile app makes it easy for you to make the most out of their funds.

An FSA is an employer-owned account that you use to set aside funds for qualified expenses. You can enroll in an FSA during open enrollment, when you’re hired, or when you experience a status change. We offer four common types of FSAs:

You can save on eligible expenses with a flexible spending account. For example, if one employee is enrolled in a medical FSA, he or she reduces the taxable income, which reduces the amount subject to Social Security and Medicare. You won’t need to pay Social Security or Medicare tax on the funds going into the FSA.

Yes! But there are restrictions. If you participate in an HSA, you can also participate in a limited medical FSA, a combination FSA, or a dependent care FSA. You can’t participate in an HSA and a general-purpose medical FSA. There are perks to participating in both accounts.

The IRS’ use-or-lose rule states that FSA funds must be spent by the participant within the FSA’s plan year. That means FSA participants typically need to spend most or all of their FSA funds by the end of the plan year. Unused funds at the end of the plan year are forfeited to the plan.

The use-or-lose rule doesn’t apply to HSAs. All HSA funds carry over from year to year.

Watch the below video from our Benefits podcast to hear from Rida Wong of Health-E Commerce about the primary differences between an HSA and an FSA.

When it’s time to choose your annual benefits, you might be weighing the options between a HSA and an FSA. Both of these accounts have a common goal: They help you make the most of your money by allowing you to put aside pre-tax dollars for qualified medical expenses.

Here are three important questions to think about as you decide which account is the right fit for you:

Answer: One of the main differences between these accounts boils down to your health plan preference and eligibility. To be eligible for an HSA, you need to be enrolled in an HSA-qualified health plan (or high-deductible health plan).

On the other hand, an FSA can work with almost any type of health plan, as long as your employer offers an FSA. When choosing the right health plan, keep in mind that:

Answer: One significant advantage of an FSA is that you can access the entire annual contribution amount right at the beginning of the plan year. For example, if you plan to contribute $2,000 to your FSA next year, you’ll have the full $2,000 available on Day 1 of the plan year.

In simple terms, FSAs work somewhat like a cash advance from your employer for eligible medical expenses. However, there’s a catch with this setup. Any funds left in your FSA at the end of each plan year, and unused money goes back to your employer. In other words, FSAs follow a “use it or lose it” rule.

Some employers offer a carryover or grace period to give their FSA participants more flexibility in spending down their funds. Be sure to review your plan documents to understand what’s offered.

In contrast, all HSA funds carry over from year to year. You get to keep your money in your account, even if you change jobs, switch health plans, or retire. Unlike an FSA, an HSA is an account that you own as a participant.

Answer: Lastly, HSAs offer a fantastic opportunity to invest the funds in your account. FSAs, on the other hand, don’t provide this investment option, so the money you put in is what you get.

This makes HSAs appealing to many members who see them as a complement to their retirement savings, alongside their 401(k). Similar to a 401(k), you can make pre-tax contributions to your HSA and enjoy tax-free growth on your investments. What’s even better is that you can take tax-free distributions from your HSA anytime you need to pay for qualified medical expenses. In contrast, distributions from a 401(k) are typically taxed as regular income, and there are often age restrictions.

Answer: Your choice between an HSA and an FSA will significantly impact your control over healthcare funds. HSAs provide more control since they are portable and belong to you, allowing you to take them from job to job and invest the funds for potential growth.

FSAs, on the other hand, are typically tied to your employer, and the “use it or lose it” rule applies to most expenses, meaning you forfeit any unused funds at the end of the plan year. So, if you prefer greater control and long-term flexibility, an HSA may be the better option, whereas an FSA offers a bit less control but can still be beneficial for covering immediate healthcare costs.

When it comes to choosing between a HSA and a FSA, there’s no one-size-fits-all answer. Your decision should align with your unique circumstances and preferences. Consider your health plan, your need for immediate access to funds, and your interest in investment opportunities. Both HSAs and FSAs have their advantages and limitations. By weighing these factors carefully, you can make an informed choice that best suits your financial and healthcare needs.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own counsel.