Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

As more and more people around the world are being vaccinated against the COVID-19 pandemic, it can feel to some like a return to normalcy is just around the corner. Unfortunately, this kind of positive thinking isn’t accurate across the board.

Even as vaccines are being administered at an increasing pace, unemployment claims have continued to rise sharply. Between November 2020 and January 2021, the number of those without jobs escalated, hitting the leisure and hospitality sectors the hardest. 110,000 restaurants have closed permanently during COVID and 500,000 others are experiencing serious trouble. More than 10.7 million people remain out of work and the unemployment rate sits at a relatively high 6.7 percent.

“The latest data points to the fragility of the recovery as the Covid crisis worsens,” said Gregory Daco, chief U.S. economist at Oxford Economics. “If this trend continues, it’s an indication that the labor market recovery has gone into reverse.” Near the end of last month, unemployment claims exceeded one million for the first time since July, with no sign of abating.

Companies are continuing to lay people off: 140,000 people were laid off in December alone. As we discussed in our first article in this series, large-scale layoffs mean that companies have to adapt the way they operate. To offset this impact on resources, companies are turning to digitization and technological innovation.

As discussed in our first article in this series, WEX worked with (E) BrandConnect, a commercial arm of The Economist Group, to survey several hundred executives in the financial services sector to investigate whether payment processes were changing in response to the pandemic and resultant economic downturn. They discovered that digital payments had reached a tipping point: “The findings show both opportunity and peril around payments, highlighting a stark reality: financial services companies that don’t adapt may not survive.”

In this five-part series, we delve into their research findings and decode the opportunity and peril highlighted in the report. In the first article, we outlined how the digital payments transformation was accelerated by the pandemic. In this segment, we’ll look at what (E) BrandConnect refers to as “the agility imperative” and how being agile will allow companies to survive the bumpy road we’re on all the way through to recovery.

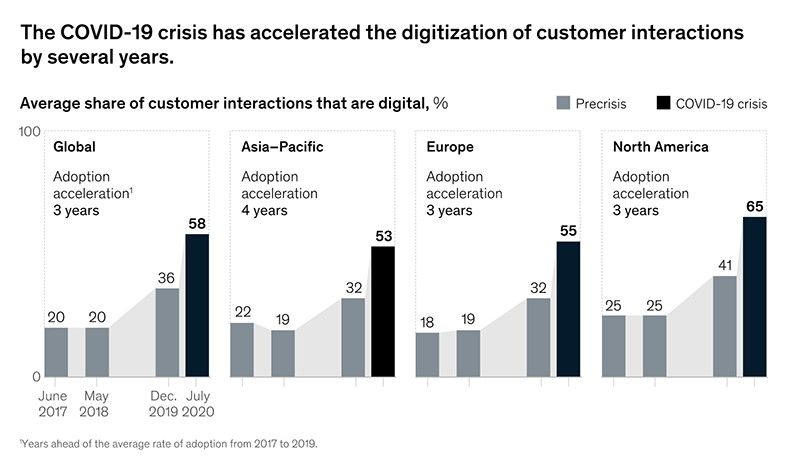

In March of 2020 when lockdowns went into effect around the world, many companies were able to continue operating as employees transitioned into working from home. Companies that were able to pivot quickly were at an advantage. A survey by McKinsey & Company showed that responses to COVID-19 sped up the adoption of digital technologies by several years. The researchers at McKinsey predict that many of the changes made over the course of 2020 are here to stay. According to executives surveyed by McKinsey, they “have accelerated the digitization of their customer and supply-chain interactions and of their internal operations by three to four years. And the share of digital or digitally enabled products in their portfolios has accelerated by a shocking seven years.”

The study conducted by WEX and (E) BrandConnect determined that simply adopting new technologies will not be enough for companies to survive post-pandemic. Instead, companies will need to pair technological innovation with “an agility mindset.” This means a shift in approach where being nimble and agile is the predominant motivating factor when making business decisions.

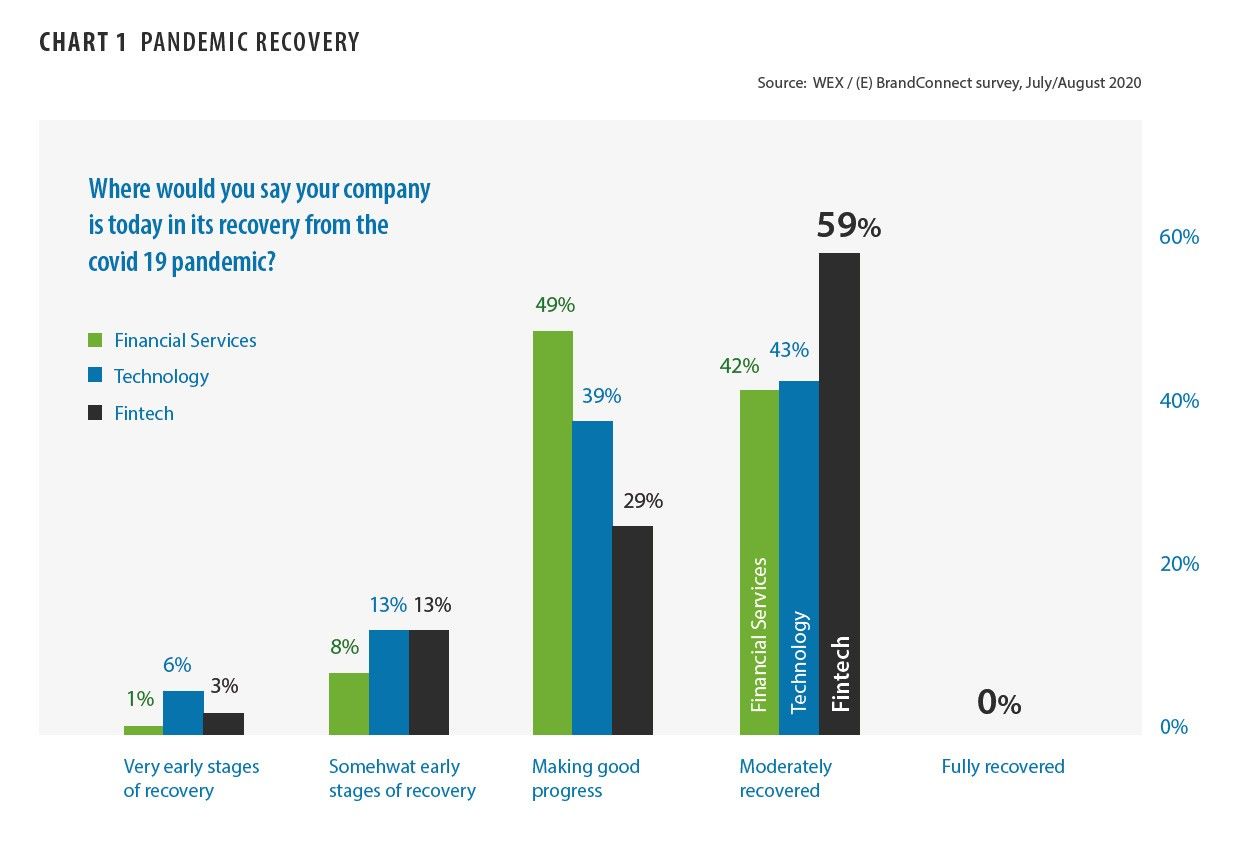

According to the (E) BrandConnect survey, the level of recovery experienced by businesses following the economic recession differed across industries. Financial services, technology, and fintech companies described divergent experiences of recuperation. All respondents indicated that COVID-19 had impacted their businesses. While no respondents replied that they were fully recovered, fintech companies experienced the most solid recovery with 59% saying they were “moderately recovered.” For technology companies, that number was 43% and for financial services companies, it was 42%.

Pandemic Recovery of Fintechs, Financial Services Firms, and Technology Companies

Fintechs, of the three groups surveyed, are the most grounded in advanced technology, meaning they were best prepared for physical lockdown. The detrimental impact of the unexpected turn to remote work was not nearly as significant for fintech companies as a result. B2B fintechs saw an even greater benefit because most of their client base shared the very same digitized systems.

The report also notes that the “link between digitization and resilience to the economic impact of COVID-19 can be seen across industries,” not just in the financial sector. For instance, digitization aided in rehabilitating the decimated retail industry. The pandemic accelerated the transition from in-store shopping to e-commerce, a metamorphosis that has been developing for more than two decades, which was suddenly thrown into hyperspeed as in-person shopping became perilous.

A report conducted by IBM explored COVID’s significant impact on retail, indicating that department store revenue declined by over 60% in the last year. Simultaneously, e-commerce grew by more than 20% in 2020. According to the (E) BrandConnect/WEX report, in just a few months of work, retailers transformed their business in ways that would normally require three to five years of operational transitioning. This move to digitizing their businesses was necessary to weather the pandemic.

Against all odds, new businesses have grown even as the virus spread. (E) BrandConnect’s research found that the impacts of COVID-19 on the global economy have created new opportunities for businesses to be born in the digital space.

Where there are new digital businesses, there are also fresh opportunities for the banking industry to roll out innovative products and services. Nascent, COVID-born companies generate revenue for the institutions that support their growth.

While the US economy has contracted by 32.9% during COVID, companies like Azlo, a business-development fintech, have had the opportunity to create new products and services tailored to these fledgling enterprises. Azlo’s CEO Cameron Peake says they’re on track to grow 300% during the pandemic, in large part due to the digitization occurring across sectors.

Start-ups are inherently flexible because they are free of onerous, ingrained processes which must be shed in order to adapt. This flexibility has given them an agility advantage. In the (E) BrandConnect report, of those surveyed, 65% of fintech respondents identify themselves as start-ups.

The student financing start-up Blair is a great example of the adaptability of start-ups in response to the pandemic. As the report describes, pre-COVID, Blair was a B2C business dealing directly with students who were seeking financial support. As the spread of the virus began to impact students and their colleges and universities, Blair saw a shift in demand and was able to pivot and react quickly and effectively. Educational institutions saw Blair as a great technological platform on which to engage with their student populations and as Blair was approached by more and more of these types of educational organizations, Blair shifted their focus away from business to consumer over to B2B to B2C. They embraced the change that came from living and working during a pandemic and adapted their business model accordingly. Their business model still requires that they provide an excellent customer experience for students, the shift is that their clients are now the institutions for which the students will need financial assistance to attend.

While start-ups have the agility advantage, companies of every shape and size have had to adapt and become more digitally dexterous as a result of the pandemic. The expression, “Innovate your way out of the crisis,” has taken on new meaning. Companies have been adapting, but as we see a possible end to this crisis in sight, the question on many industry analyst’s minds is whether or not companies will be able to sustain this new level of technological advancement. As we move to a post-pandemic world, company leaders must maintain a focus on digitization and the expansion of their technological infrastructures. As the Harvard Business Review points out in a recent article, “The pandemic has pushed societies to an inflection point where embracing technology is no longer an option but a necessity.”

There are some signs that indicate technological advancement will not abate post-COVID. One such indicator is the vast leap in investment in bot technology over the last 12 months. The number of robots operating worldwide is rising rapidly. By the end of 2020, there were three million new industrial robots in operation. This is more than double the number of robots operating between 2014 and 2020. When companies invest in robotics, they are committing themselves to the use of these mechanisms, and are not likely to revert back to human-run operations.

Another powerful indicator that technological advancement will be a continued focus for businesses when the pandemic is under control is this simple fact: companies have grown when they have focused on implementing digital processes. When new ways of operating through the use of digitization are introduced, companies can experience opportunities to develop and build their business in ways that would not have been possible if they had not embarked on technological advancement. To ignore these developments would only bring about weaker security and reduced growth. Companies across sectors know that it will be wisest to continue down the technological path on which the pandemic has started us.

Digitization is a critical factor for companies to survive the COVID-19 pandemic. Of those surveyed by (E) BrandConnect, a clear majority (84%) felt confident in their digital infrastructure and believed it would see them through to the other side of the pandemic. These companies have their IT teams’ resilience, resourcefulness, and adaptability to thank for their confidence that they’ll survive one of the worst economic crises in the last hundred years. If it weren’t for impactful investments made by IT professionals in cloud computing, many of these companies would be struggling or out of business today.

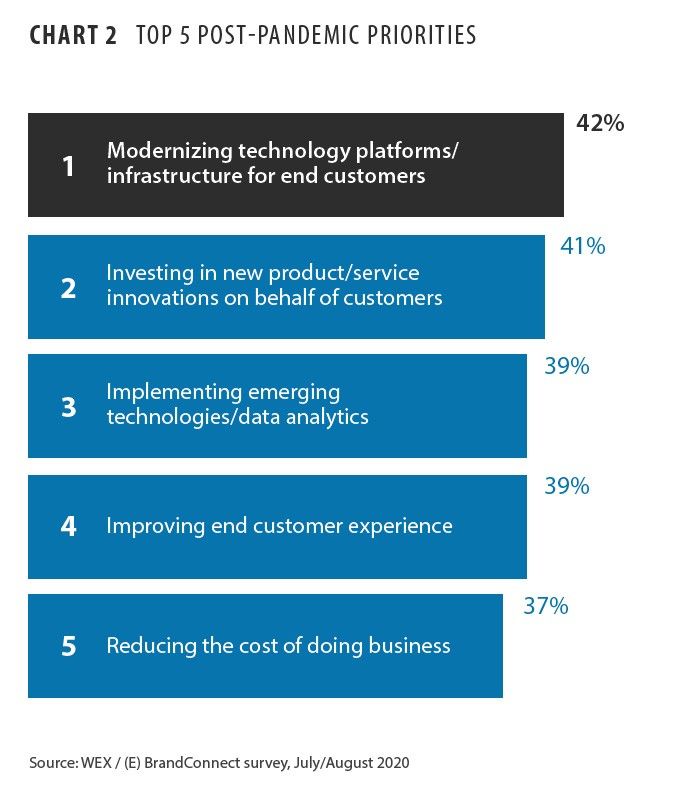

While the survey shows confidence in infrastructure, what it does not communicate is a sense that participants feel that their digitization work is done. When those same companies were asked what their top strategic priorities were as the economy recovers, the most common answer was “modernizing technology platforms/infrastructure for end customers.” Another popular response was “implementing new technologies/data analytics.” Executives are prioritizing technological innovation and data analysis because that technology is constantly changing, and the types and sizes of data are constantly changing and to stay competitive they need to continue innovating. Innovative, smart companies are aware of the need to work with newly developed, efficient tech, and at the same time, these companies are aware of the importance of prioritizing adaptability when developing future strategies.

Top Five Post-Pandemic Priorities for Those Surveyed

A prime example of the need for adaptability is in the payments industry. Outdated processes were strained globally when most of the world’s workforce shifted to remote work. As Greg Sassone, senior vice-president of business and partner growth at WEX explains, “Legacy processes and platforms don’t perform well in a work-from-home environment.” A large proportion of businesses were still cutting paper checks, and handling payments with outdated, manual processes pre-COVID. As the virus took hold, companies needed to innovate their payments processes quickly to adjust to remote work and pared-down resources. The companies that were able to adapt quickly from paper-based processes to virtual payments experienced the least amount of hiccups and customer dissatisfaction, compared to those which did not modify their payment systems.

As the (E) BrandConnect report illustrates, companies are aware of the need to continue to innovate and digitize even after vaccinations become available for wider and wider segments of the population, and work returns to in-person. Eighty-six percent of respondents felt that “companies that lead with technology will thrive in recovery from the current economic and health crisis,” and 80% thought that “companies that continue to lag behind on internal technological infrastructure changes will be left behind.” The starkest statistic from the report is that 82% of respondents believe that “companies that have fallen behind on their digital transformation will soon be obsolete.”

Beyond the miraculous impact of digitization on suffering businesses during the lockdown, companies are beginning to see digitization as a way to generate new sources of revenue. Sassone says, “Adopting digital payments not only helps with efficiency but companies can actually earn rebates from providers in order to monetize those payments.” With faster, more efficient payments, companies can take advantage of things like early payment discounts. Digital payments can also sometimes come with additional financial incentives. There might be discounts related to interchange fees that work in a payers’ favor, for example.

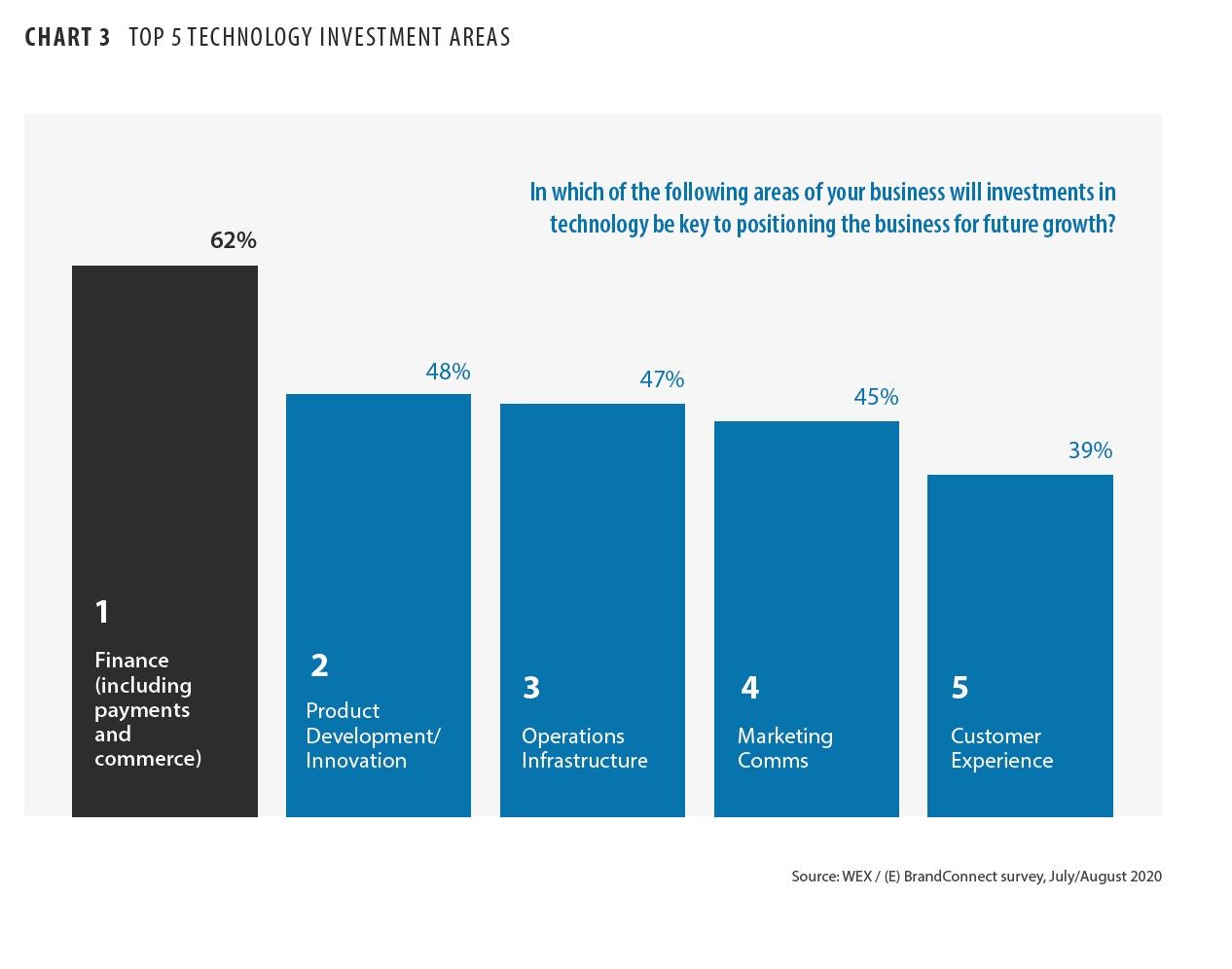

Executives surveyed by (E) BrandConnect indicated that they will continue to innovate and digitize and they suggested that the most likely place they’ll direct their digitization efforts will be in the realm of finance, including payments and commerce. Financial digitization is where their budgeting dollars will go and where their strategic goals will be directed. For financial service providers (68%) and fintechs (64%) to direct budgeting dollars toward advancements in payments technologies seems like the obvious and appropriate course of action. The less obvious response came when tech companies also indicated an interest in investing in payments technologies. Fifty-five percent of technology companies suggested that they would be focused on financial technology as a priority going forward.

Advanced payments technology provides companies with an opportunity to help their customers sustain and initiate agility post-pandemic. By providing digital solutions, these companies are giving their customers an edge over their competitors. The old ways of processing payments, using paper and human capital, are a thing of the past. Digital transformation is the future of payments.

Top Five Technology Investment Areas Post-COVID

A recent Forbes article predicts we won’t see a full economic recovery until well into 2022, and the International Monetary Fund has predicted that the global economy will lose over $22 trillion between 2020 and 2025. As we weather the coming months, making our way carefully towards COVID vaccination and beyond, championing innovation will help you, your companies, and your employees land on their feet in a post-COVID era.

Stay tuned for the next installment in this series where we take a deep dive into how companies can capitalize on the payments opportunity wrought by the COVID pandemic.

Click here to learn more about how WEX payment solutions can be tailored to your business, so you can operate easier and faster while creating lasting growth and success.

Click here and scroll down to the yellow icon to download and read the full Economist white paper, “The Digital Payments Tipping Point.”

Resources:

New York Times

McKinsey & Company

TechCrunch

Economics Observatory

Bloomberg

Harvard Business Review

CNN

Forbes