Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

The IRS requires your flexible spending account (FSA) participants to submit documentation to prove their purchase was an eligible expense. The IRS emphasized these requirements and potential penalties for employers not meeting the requirements when releasing an Office of the Chief Counsel memorandum detailing medical expense claim substantiation for medical FSAs and dependent care FSAs.

That’s why you need an FSA administrator that adheres to IRS substantiation requirements and offers innovative solutions to simplify the substantiation process for your employees. Keep reading to learn more about why the IRS substantiation guidelines are important and what you and your participants can do to stay in compliance.

Because of an FSA’s tax advantages, the IRS requires employers and employees to prove that FSA funds are only being spent on eligible expenses.

FSAs are a great way for employers and employees to save. When employees participate in an FSA, employers save on FICA taxes since their participation reduces their taxable wages. And they save because the funds they contribute and their reimbursements for eligible expenses are not taxed.

FSAs are employer-sponsored accounts, so it’s particularly important for you to comply with IRS regulations regarding documentation. If the IRS determines your FSA is or was not in compliance with substantiation requirements, your FSA could become disqualified.

Last year’s memorandum states that any FSA not following substantiation rules does not comply with IRS Code Section 125 and any employee contributions to a noncompliant plan is subject to income, FICA, and FUTA taxes. In some circumstances, the IRS could treat all medical FSA reimbursements within a noncompliant plan, including those that were properly substantiated, as taxable wages and subject to FICA and FUTA taxes.

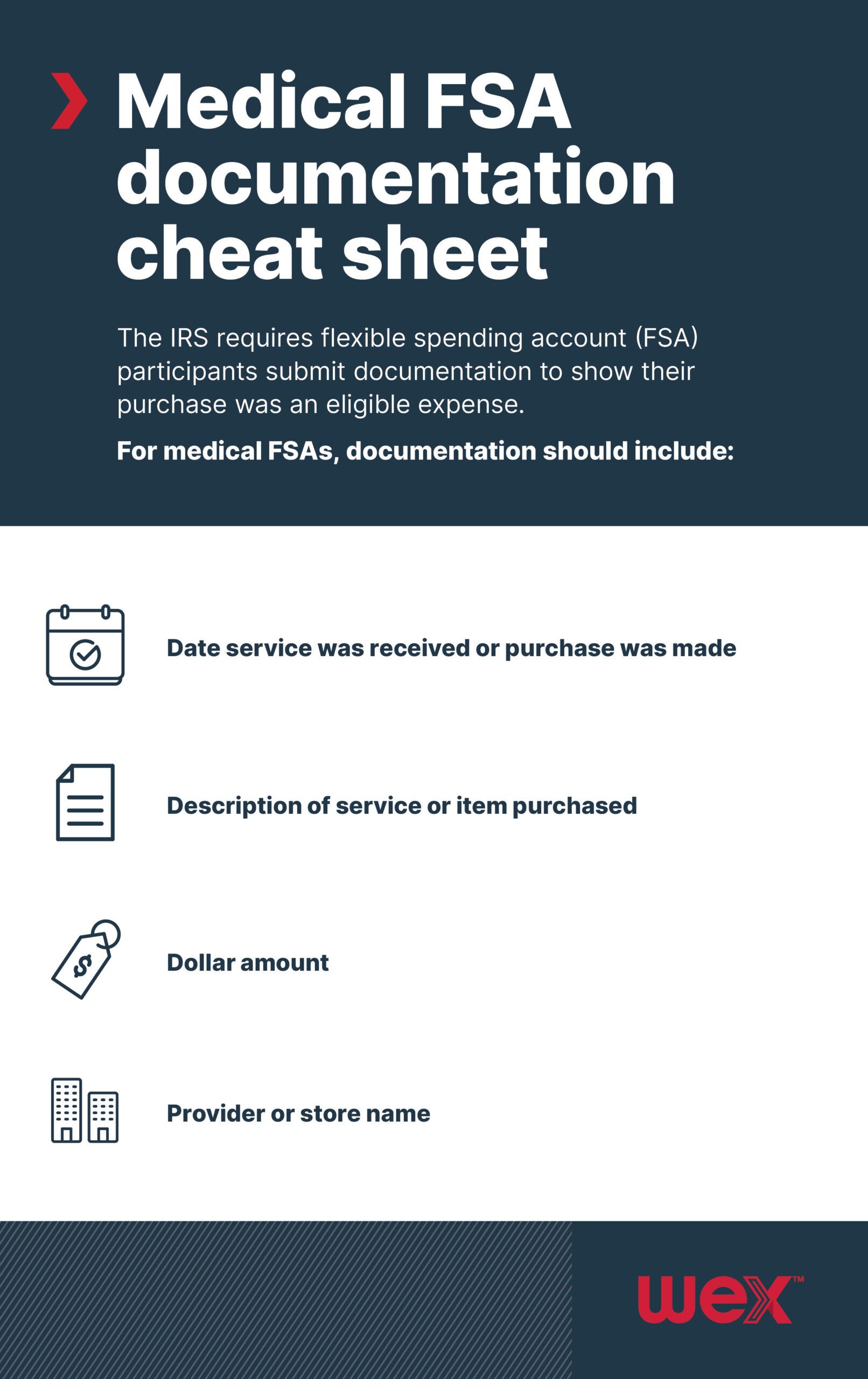

To reduce your risk as an employer and the potential for future financial headaches, choose a third-party administrator that requires claims to be substantiated. IRS regulations outline what your employees’ documentation should contain. For medical FSAs, documentation should include:

An Explanation of Benefits (EOB) typically contains the information required by the IRS.

When you’re choosing your third-party administrator, look for one with a proven track record of making the process of submitting substantiation as easy as possible for your employees. For example, participants with an FSA powered by WEX have access to technology, processes, and educational materials to make it easier for them to access their funds. That includes:

Would you like to learn more about FSA substantiation? Check out the below FSA documentation cheat sheet.

This blog post was most recently updated in April 2025.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own legal counsel, tax and investment advisers.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.