Stay connected

Subscribe to our health benefits blog and follow us on social media to receive all our health benefits industry insights.

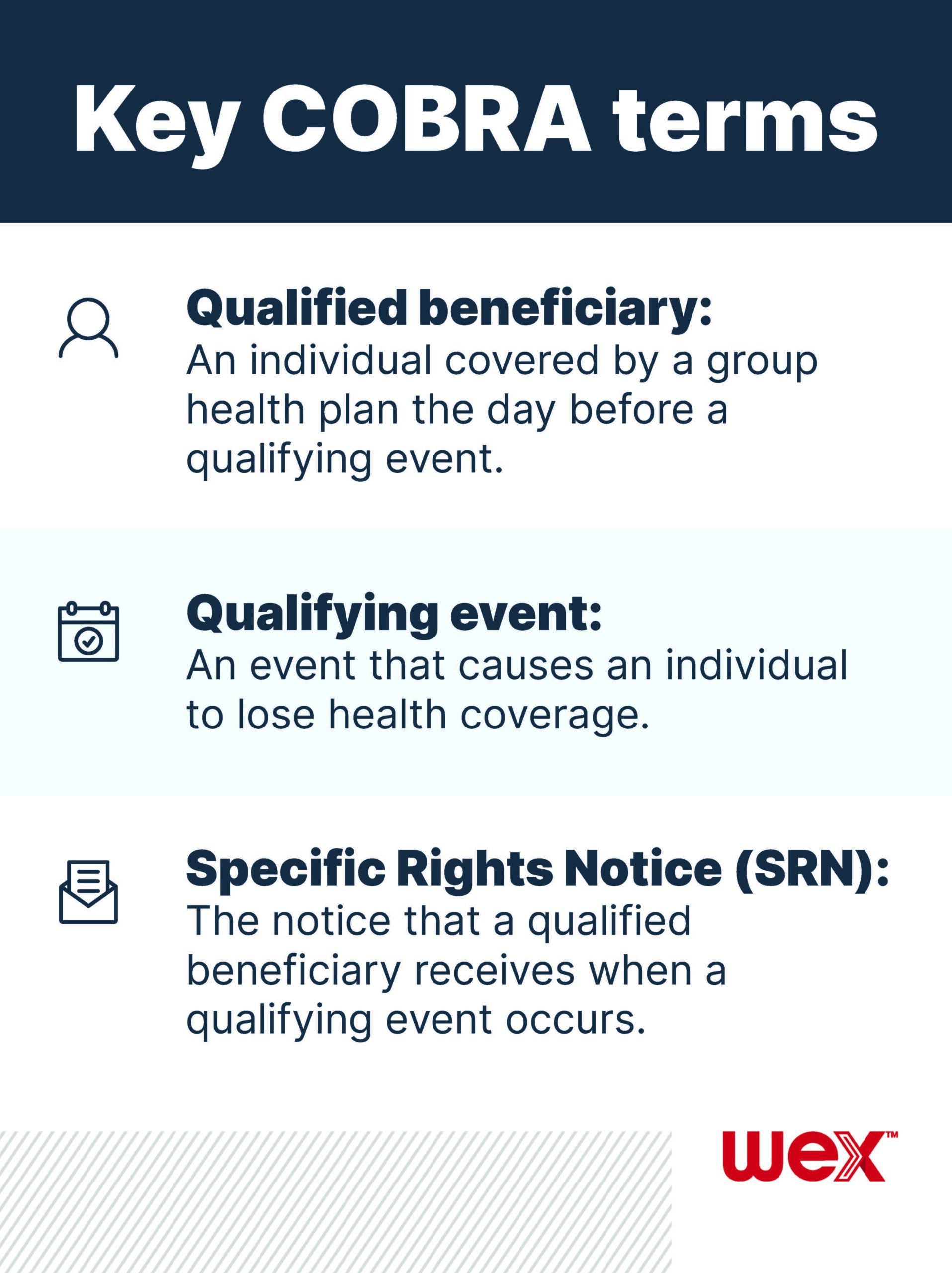

COBRA health insurance gives your qualified beneficiaries the opportunity to continue to be enrolled in the same health coverage they were enrolled in when the qualifying event interrupted their coverage. But not every employer is required to offer temporary health insurance. And, since COBRA is federally regulated, it’s important to know when it needs to be offered and for how long. Learn the answers to the following common COBRA regulation questions to determine how you’re impacted by the long-standing federal law.

If you employ at least 20 people, then you’re likely required to provide COBRA to your qualified beneficiaries. A few factors to consider include:

If your business/organization is required to offer COBRA coverage, then you must offer it to an individual who lost coverage in your group health plan after they experienced a qualifying event. Qualifying events include:

Additionally, spouses or dependent children need to be offered COBRA if one of the above or following events impacts their coverage:

You have 30 days to notify your plan administrator that a qualifying event has occurred. Within 14 days of notification, your plan administrator must mail a Specific Rights Notice (SRN) to the individual who is now eligible for COBRA. From there, it’s in the hands of the qualified beneficiary to decide whether or not to elect COBRA.

COBRA health insurance premiums can’t cost more than the cost of coverage through the group health plan, plus a 2% administration charge. Employees typically pay the entire cost of COBRA coverage, but an employer can opt to pay for a portion of coverage under certain circumstances. You can also save you and your employees money by offering coverage through a COBRA alternative marketplace.

You’re required to provide COBRA coverage for 18 or 36 months, with the length of time determined by the type of qualifying event that occurred. For example, when the qualifying event is an employee’s termination or reduction in hours, you’re only required to offer continuation coverage for 18 months. Most other qualifying events require 36 months of coverage to be offered, but there are variables.

Stay up to date on the latest with COBRA by subscribing to our blog!

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own legal counsel, tax and investment advisers.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.