Stay connected

Subscribe to our health benefits blog and follow us on social media to receive all our health benefits industry insights.

"*" indicates required fields

It’s 2023! To kick off another year of providing you with the employee benefits tips and information you need, we wanted to look back at your favorite blog posts from the last year. Here are our top 10 blog posts from 2022:

Were you among the 20% of workers expected to quit their jobs in 2022? Fortunately, your health savings account (HSA) is an employee-owned account, so it stays with you, even when you switch employers. Check out our blog post and podcast episode to learn more about your HSA options when you change jobs.

An HSA comes with three key tax-free perks: Contributions are tax-free, earnings are tax-free, and withdrawals for eligible expenses are tax-free. Considering how much the average American is expected to need to cover healthcare costs in retirement, you might be wondering how much you should contribute to your HSA. This blog post will help you decide.

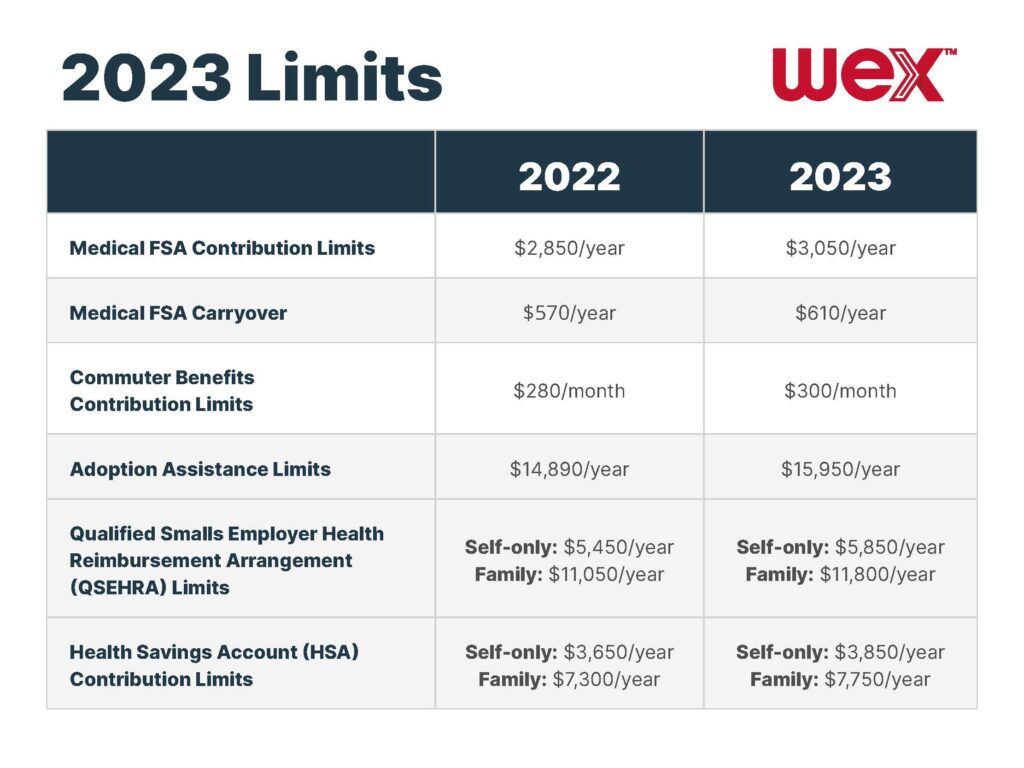

The IRS announced significant increases to HSA contribution limits in 2023 as a result of rising inflation. Self-only HSA participants can contribute up to $3,850, while family HSA participants can set aside $7,750 in 2023. And those who qualify for catch-up contributions can add an additional $1,000 to those limits. Learn more about the limits here.

Did you know that you can participate in both an HSA and a flexible spending account (FSA)? It’s true! But it’s important to know that this applies to only certain types of FSAs. Check out this blog post and watch our podcast episode to learn more about limited FSAs and why they’re the perfect complement to HSAs.

The IRS’ use-or-lose rule is the reason why FSA funds must be spent down by the end of the plan year. What happens when funds aren’t spent by the end of the year? And how does it affect FSA carryovers? Find out in our blog post.

Nearly two-thirds of parents say that childcare costs have risen in the last year. One way to combat these rising costs and save money is to participate in a dependent care FSA. Dependent care FSA participants can save on eligible childcare, elderly care, and other dependent care costs. Learn more about these plans and how much you can contribute to a dependent care FSA.

2023 contribution limits for FSAs, commuter benefits, and other plans also increased considerably due to inflation. For example, the medical FSA contribution limits rose to $3,050 for 2023, which is a $200 increase from 2022. Find out more about these limits, as well as limits for QSEHRAs and adoption assistance.

If your FSA has a grace period, you may still have time to spend down your remaining balance from your 2022 FSA. Need a few tips on how to spend down your remaining FSA funds? We’ve got you covered in this blog post.

The Affordable Care Act (ACA) provides specific direction on reporting medical benefits offerings to employees. Get a breakdown on these codes to better understand how you can remain in ACA compliance.

The IRS requires non-discrimination testing of any benefits plans governed by Section 125. FSAs and health reimbursement arrangements (HRAs) are just two types of benefits where testing is mandated. When should you test? And who is responsible for testing? We cover it all in this blog post.

Stay up to date on the latest trends in employee benefits by subscribing to our blog! Simply submit your email address on the right-hand side to receive email alerts when we publish a new blog post.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own legal counsel, tax and investment advisers.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.